Global Space Launch Services Market Set to Soar: Comprehensive Analysis Reveals Robust Growth and Emerging Opportunities

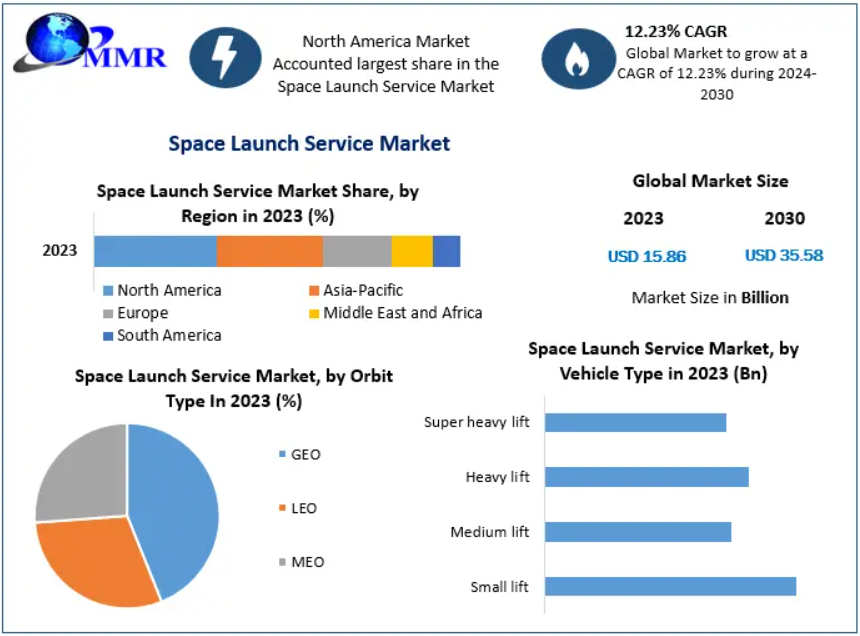

The Global Space Launch Services Market Size is on a trajectory of significant expansion, propelled by technological advancements, increasing commercial investments, and a burgeoning demand for satellite-based applications. Recent analyses project the market to grow from USD 15.86 billion in 2023 to an impressive USD 35.58 billion by 2030, reflecting a Compound Annual Growth Rate (CAGR) of 12.23%.

Market Definition and Estimation

Space launch services encompass the comprehensive suite of operations required to transport payloads—such as satellites, cargo, and crewed missions—into space. These services include pre-launch activities (mission planning, payload integration), launch execution (vehicle launch, trajectory management), and post-launch operations (payload deployment, telemetry analysis). The escalating reliance on satellite technologies for communication, navigation, Earth observation, and scientific research underscores the critical role of efficient and reliable launch services in the modern aerospace landscape.

For in-depth information on this study, visit the following link:https://www.maximizemarketresearch.com/request-sample/1708/

Drivers of Market Growth and Emerging Opportunities

Several key factors are fueling the robust growth of the space launch services market:

1. Proliferation of Satellite-Based Applications

The surge in demand for satellite-enabled services—including broadband internet, global positioning systems (GPS), and environmental monitoring—necessitates the deployment of advanced satellite constellations, thereby driving the need for frequent and cost-effective launch services.

2. Commercialization and Private Sector Investment

The entry of private enterprises into the space sector has revolutionized launch dynamics. Companies have introduced reusable launch vehicles and cost-efficient solutions, significantly reducing the financial barriers to space access and stimulating market growth.

3. Advancements in Launch Vehicle Technology

Continuous innovations in launch vehicle design, propulsion systems, and materials have enhanced payload capacities and reliability. The development of reusable rockets has been pivotal in lowering launch costs and increasing launch frequency.

4. Emergence of Space Tourism

The nascent space tourism industry presents new avenues for market expansion. Companies are pioneering sub-orbital flights for private individuals, indicating a promising diversification of launch service applications.

In-Depth Segmentation Analysis

The space launch services market is segmented based on payload type, launch platform, launch vehicle class, end-use sectors, and geographic regions.

By Payload Type

- Satellites: This dominant segment caters to various functions, including communication, Earth observation, and navigation. The miniaturization of satellite technology and the deployment of large-scale constellations have intensified launch demands.

- Cargo Resupply Missions: Essential for transporting supplies to the International Space Station (ISS) and future space habitats, this segment ensures the sustainability of long-duration missions.

- Crewed Spaceflights: Human space exploration and commercial astronaut missions fall under this category, highlighting the expanding scope of human presence in space.

By Launch Platform

- Land-Based Launches: Conventional launch sites provide established infrastructure and logistical support, accommodating a wide range of missions.

- Airborne Launches: Air-launch systems offer flexibility in launch locations and trajectories, enabling responsive deployment capabilities.

- Sea-Based Launches: Maritime platforms facilitate equatorial launches and mitigate overflight risks, enhancing operational versatility.

By Launch Vehicle Class

- Small Launch Vehicles: Designed for lightweight payloads, these vehicles support the growing market for small satellites and rapid deployment needs.

- Medium to Heavy Launch Vehicles: Capable of carrying substantial payloads, they are integral to deploying large satellites and interplanetary missions.

By End-Use Sectors

- Government and Military: National security satellites, scientific research missions, and strategic defense initiatives are primary drivers in this sector.

- Commercial Enterprises: Private companies focusing on telecommunications, Earth observation, and emerging space tourism ventures represent a rapidly expanding customer base.

Country-Level Analysis: United States and Germany

United States

The U.S. maintains a leading position in the global space launch services market, attributed to substantial investments in space exploration and the presence of pioneering companies. Government agencies like NASA and the Department of Defense continue to be major stakeholders, funding a diverse array of missions that bolster the domestic launch service industry.

Germany

As a key player in the European space sector, Germany contributes significantly through its involvement in the European Space Agency (ESA) and national initiatives. German aerospace firms are integral to collaborative projects, enhancing Europe's competitive stance in the global market. The country's focus on technological innovation and precision engineering underpins its strategic contributions to space launch capabilities.

To access more details regarding this research, visit the following webpage:https://www.maximizemarketresearch.com/market-report/space-launch-services-market/1708/

Competitive Landscape and Key Players

The space launch services market is characterized by a dynamic and competitive environment, with several key players driving innovation and market growth:

- SpaceX: Renowned for its reusable Falcon rockets and ambitious Starship program, SpaceX has revolutionized cost structures and operational paradigms in the industry.

- Blue Origin: Founded by Jeff Bezos, Blue Origin focuses on developing reusable rocket technology and has made significant strides in both sub-orbital and orbital launch capabilities.

- Rocket Lab: Specializing in small satellite launches, Rocket Lab's Electron rocket has become a preferred choice for deploying lightweight payloads, catering to the burgeoning small satellite market.

- United Launch Alliance (ULA): A joint venture specializing in reliable launch systems for government and commercial clients.

- Arianespace: A European aerospace company leading in commercial satellite launches, enhancing Europe's presence in the global launch market.

Conclusion

The global space launch services market is undergoing rapid transformation, driven by technological advancements, increasing commercial investments, and expanding applications in both government and private sectors. As space exploration and satellite deployment continue to accelerate, the demand for efficient and cost-effective launch solutions will shape the industry's future trajectory.

With innovations in reusable launch vehicles, growing international collaborations, and emerging opportunities in space tourism and deep-space missions, the market is poised for sustained growth in the coming decade. Key industry players are expected to play a crucial role in enhancing access to space, driving down costs, and ensuring that the benefits of space technology extend to various sectors of the global economy.